With the year drawing to a close and markets slipping into their usual December quiet, it feels like the right moment to take stock. Just over a decade ago, The Economist ran its now-famous “Africa Rising” cover, and investors paid generously for the promise of this African growth.

Today, Africa is broadly undervalued, priced like a distressed asset. What is emerging now looks like the early phase of a cyclical rebound that could run for a few years across assets-currencies, bonds and, increasingly, equities; driven by reforms and policy adjustments.

Across the continent, the macro backdrop is improving, albeit unevenly. FX reserves have begun to rebuild across a select group of reform-oriented economies and, barring any major external shock, should continue accumulating into 2026.

(Source: Bloomberg, RenCap Africa)

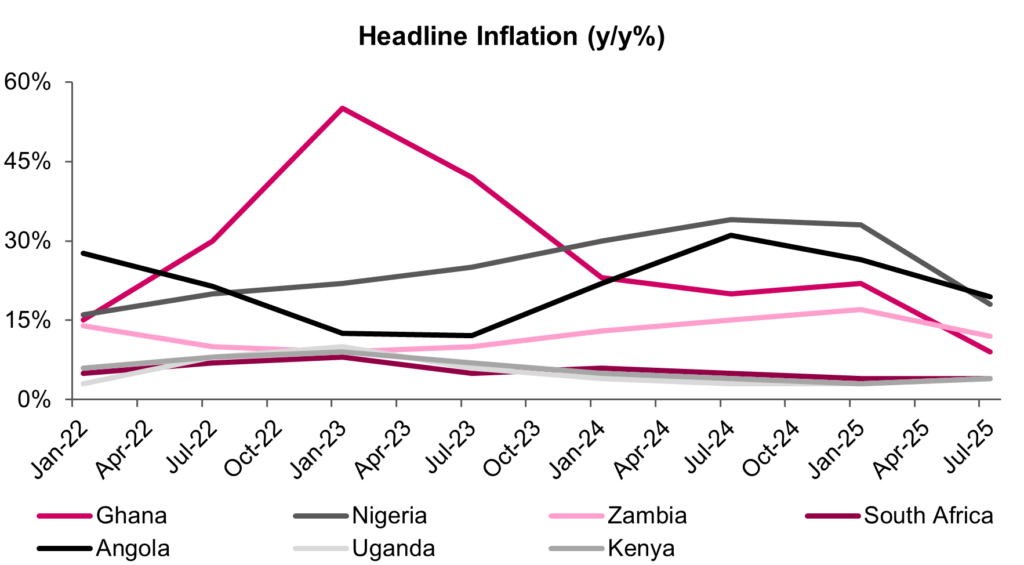

Trade dynamics are also shifting. For Sub-Saharan Africa, the EU and China now matter more than the US, cushioning the region from headline US political noise. With inflation easing, several central banks, notably in Nigeria, Egypt, Ghana and Zambia are entering or extending monetary easing cycles, setting up a more supportive environment for local bonds.

(source: Bloomberg, RenCap Africa)

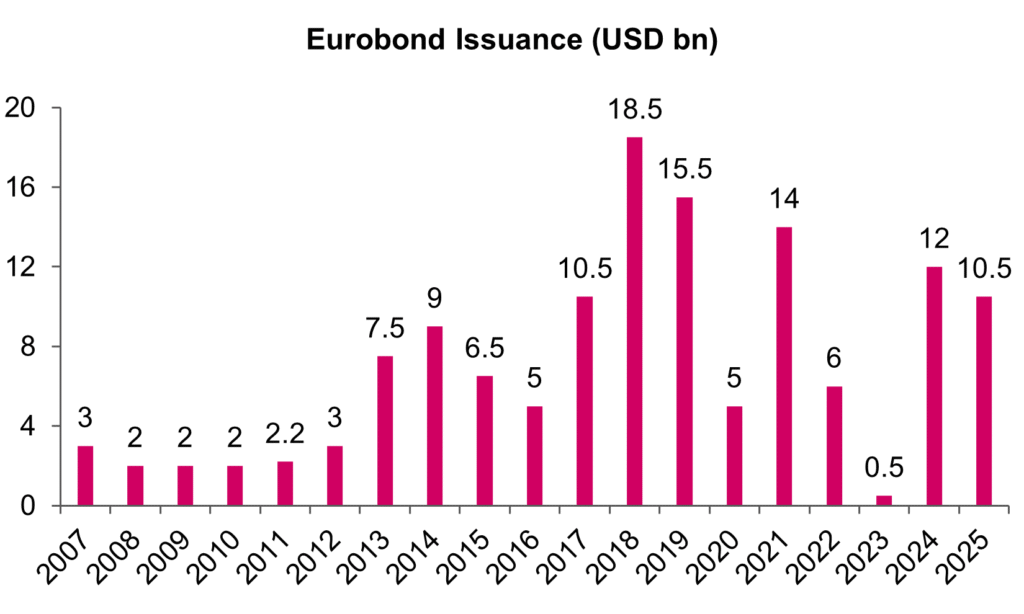

At the same time, external market access is reopening, with Eurobond issuance expected to pick up in 2026 as confidence returns.

(source: Bloomberg, RenCap Africa)

Layered on top is a busy election calendar, which will test reform credibility in some markets and reward discipline in others. The opportunity, as ever in Africa, is not uniform.

Nigeria

We expect more of the same in 2026, at least in 1H 2026, following a strong performance from the Nigerian government in 2025, at least on the monetary side. We note that the central bank has done very well to build investor confidence leading to the 37% increase in foreign currency reserves since the start of 2024, but more importantly, the quality of the reserves, and the moderation in inflation, which could drop to 13% by the end of 2026, according to the IMF. The lower inflationary pressures should allow the central bank to cut rates aggressively by 500bps+ in 2026.

All eyes will be on the fiscal authority to build on the efforts and success of the monetary authority. A revenue-led fiscal consolidation is still very much needed but may not materialise in the absence of a noteworthy increase in oil production given the risk of lower oil prices and minimal incremental increases from recent tax reforms. We do, however, acknowledge the improvement in business sentiment and efforts to boost oil and gas investments, which should result in higher production levels over the medium term. Oil price remains a key risk for the country across fiscal and external accounts, but robust external reserves and low external amortisation and service needs are comforting while risk off sentiments seem manageable. We believe the elections in 2027 pose a very low political risk given the absence of a credible opposition party and candidate.

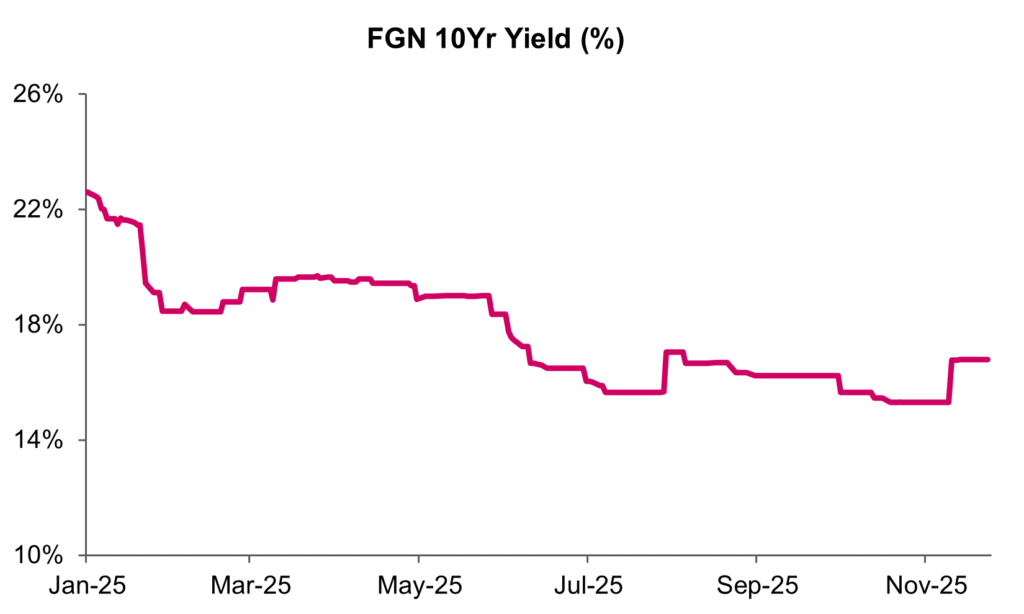

Thanks to a disinflationary backdrop and an easing interest-rate environment, Nigerian bond yields have compressed sharply, declining by roughly 600–800bps across the curve.

(Source: Bloomberg, RenCap Africa)

As disinflation continues and the policy rate trends lower, we expect further downward pressure on yields. Local bonds should therefore continue to benefit from rate cuts, with longer-duration FGN securities offering near-term mark-to-market gains.

Despite the rally, Nigeria’s local debt market still offers double-digit yields, making it highly attractive in a global context. Local bonds remain the favoured trade for international debt investors as we head into 2026, combining yield, improving macro credibility and capital-gain potential. This contrasts with the nation’s hard currency bonds, where we have a neutral stance as spreads have tightened aggressively over the last 18 months in response to improvements in the global and domestic economies with very little catalyst on the horizon. We note that an uptrend in inflation and rates in USA could see spreads unravel in 2026.

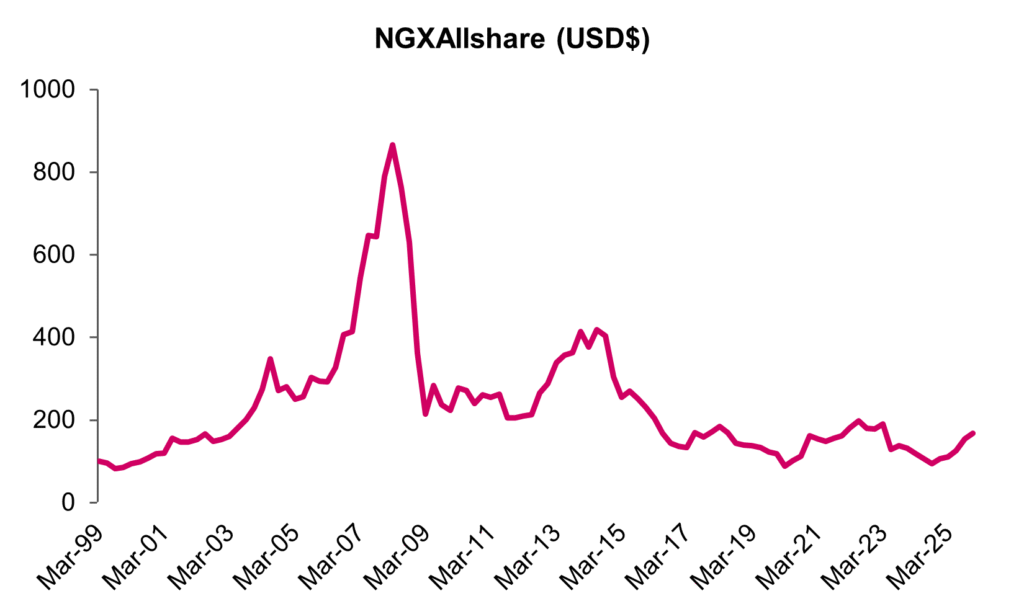

Nigerian equities are up over 50% in US dollar terms year-to-date by mid-December. Yet despite this strong rebound, the NGX All-Share Index remains more than 80% below its 2007 all-time high in US dollar terms, highlighting just how deep and prolonged the drawdown has been.

(Source: Bloomberg, RenCap Africa)

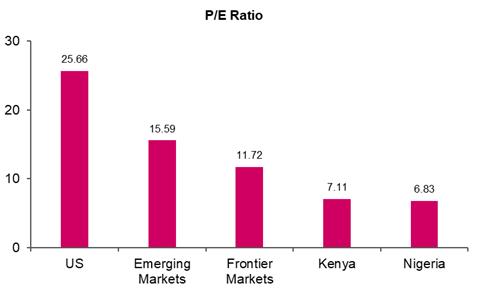

Even after the rally, Nigerian equities remain cheap relative to peers. At around 6.8x earnings, Nigeria trades at a discount to frontier and emerging market averages and at a fraction of US equity valuations, which are closer to 26x.

(Source: Bloomberg, RenCap Africa)

As FX stabilises and macro credibility improves, there is meaningful upside left to play out into 2026.

Angola

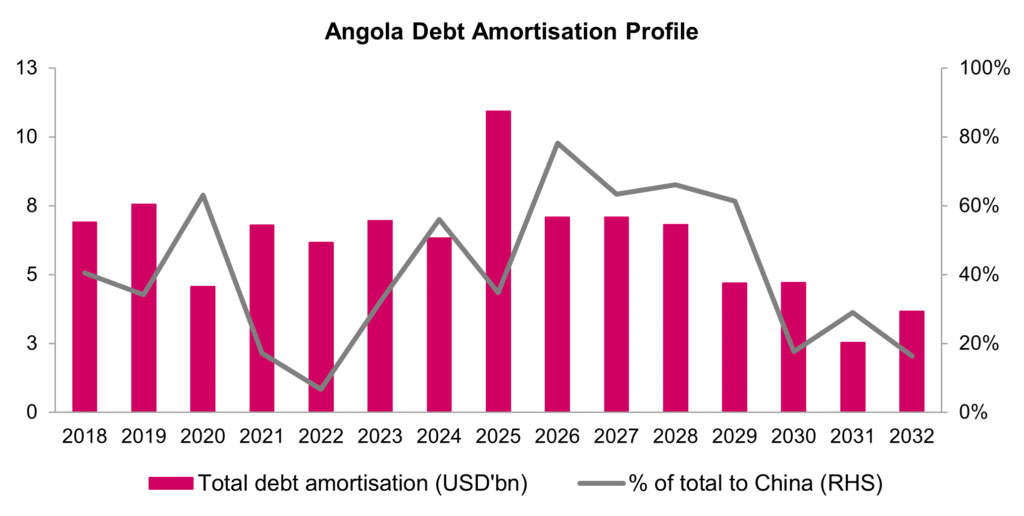

Angola heads into 2026 with the risk of a twin deficit high given its politically driven spending needs, with general elections scheduled for 2027, and lower oil production coupled with an uncertain price outlook. Access to external funding, with its first Eurobond issuance since 2022, which eliminated near term refinancing risk, and financing from DFIs have been supportive. Financing needs, however, are expected to remain elevated over the medium term, which could lead to some deterioration in foreign currency reserves despite some flexibility surrounding the repayment of oil-backed loans from China. Consequently, as electioneering activities gather momentum, reform efforts may give way to spending meaning energy subsidies will linger, growth could be challenged in 2H26 while inflation could begin to trend upwards on the back loose fiscal policy and foreign currency management and illiquidity. This combined with the risk of lower oil prices, a key source of the country’s foreign currency inflows but also has a strong correlation with long-tenor Eurobonds, leaves us to believe Angola’s hard currency bonds could underperform, particularly in the second half of 2026.

(Source: World Bank, RenCap Africa)

Kenya

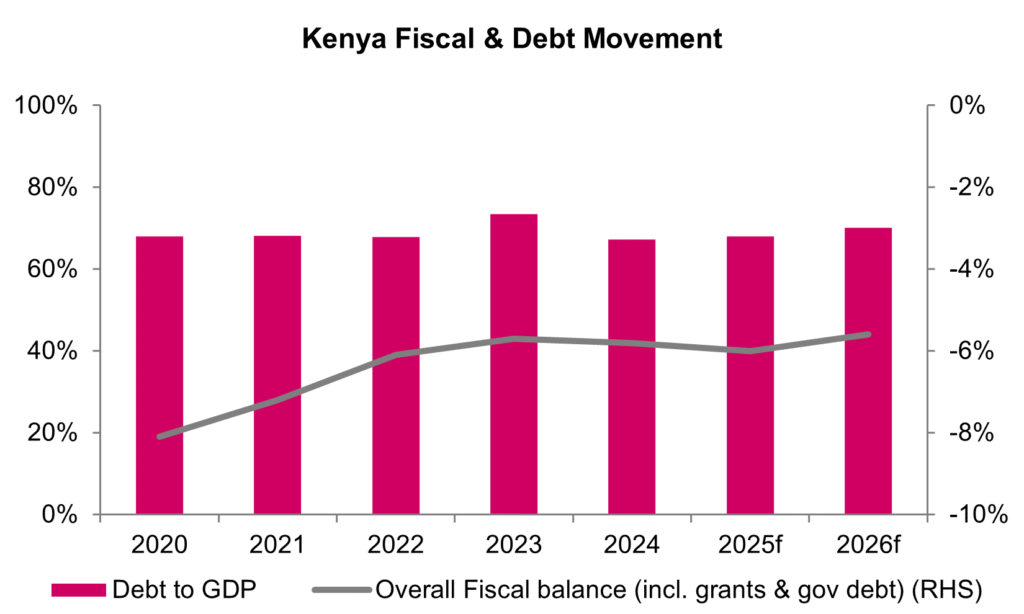

The authority’s fiscal trajectory will likely remain a key concern for stakeholders in 2026. The liability management exercise over the last 18 months has bought the government some breathing space on debt amortisation, with some benefits on debt servicing as well. Furthermore, stronger foreign currency reserves with lower oil prices on the horizon, should support external accounts over the medium term while inflation should remain within target band. However, policy credibility on the side of the fiscal authority combined with high risk of social unrest means reforms to curb the deficit are unlikely to materialise in the near term. Recently and unsurprisingly, the authorities raised the fiscal deficit target to 5.3% for 2025/26, from 4.7% previously. A new funded IMF programme ordinarily would be positive but discussions to finalise still appear to be some distance away given poor track record independently reducing the deficit, differences on reforms and definitions around securitised revenues. The likelihood of a new programme as we move closer to the general elections in 2027 will decline, giving way to fiscal indiscipline. Nonetheless, with the recent and unfortunate passing of Raila Odinga, a key opposition party candidate, we believe the presidential election could be Ruto’s to lose, which could limit the need for election related spending and the resulting inflationary pressures. The risk of violence and social unrest linked to the elections could, however, see foreign investors flee local and foreign currency assets. Consequently, we are neutral on Eurobonds heading into 2026 and likely to be underweight in 2H26.

(source: Bloomberg)

This is the first part of a two-part series on Africa in 2026. In Part 2, we turn to more country-level stories focusing on Ghana, Egypt, Côte d’Ivoire and others and where we see value emerging as reforms take hold and mispricings persist.