Senegal

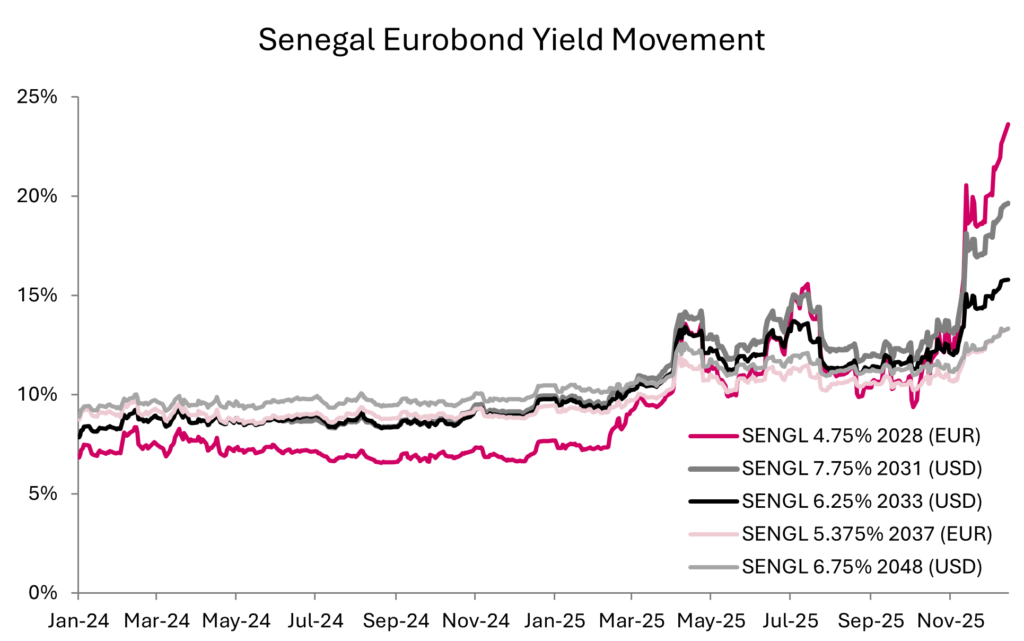

Senegal remains a divisive subject amongst stakeholders who are torn as to whether the Internation Monetary Fund will deem the nation’s debt, estimated to be over 130% of GDP as at the end of 2024, sustainable as part of consultations for a new three-year funded programme. The absence of a staff level agreement at the end of the Fund’s November visit to Senegal and the comments by Prime Minister Sonko means that a new IMF programme may still be some distance away with the Senegalese authorities utilising its alternative, albeit reducing, financing options to manage its financing needs. In a scenario that the Fund determines that the nation’s debt sustainable on a forward looking basis and a new programme is approved by the board, the fiscal consolidation efforts required could be challenging for the Faye-Sonko administration, who thus far have done very little to rein in the fiscal deficit, which was above 12% in 2024, as well as the significant risk of social unrest as subsidies will likely be reduced, new taxes introduced and tax rates increased. As such, the government performance would fall below expectations leading to hard restructuring in 2H 2026, which does not yet appear to be fully priced into outstanding Eurobond prices. As such, we hold a negative view on the bonds with the only catalyst on the horizon being a new funded IMF programme, which still appears to be some time away. Unlike Ghana, Senegal’s pegged currency will limit its ability to inflate away some of the pains, resulting in a very challenging few years for the country, which will be evident in growth and aggregate demand.

(Source: Bloomberg, RenCap Africa)

Ghana

Ghana, arguably the strongest macro turnaround story in the region. In late 2022 the country defaulted on its domestic and external debt, suspending bilateral obligations as inflation surged to 54%, the cedi depreciated sharply, policy credibility disintegrated, and reserves collapsed to $5b in 2023. The crisis forced Ghana into an IMF programme and a sweeping restructuring of both domestic and external debt. Yet the speed and depth of the recovery have surprised many market participants. Inflation, which started 2025 around 23%, has now fallen squarely within the central bank’s 8% ± 2% target range; the Monetary Policy Rate, peaked at 30% in 2024, has been cut to 18%; reserves have more than doubled to over $11 billion; and the cedi has appreciated roughly 22% this year. The 2024 elections rather than overwhelm economics or derail stabilisation, it reinforced policy continuity and commitment to reforms.

(Source: Bloomberg, RenCap Africa)

Ghana has swung from persistent trade deficits during the crisis period to a sizeable trade surplus, supported by higher gold export receipts and improved formalisation of gold flows. This external rebalancing has been central to reserve accumulation, FX stability, and the rapid restoration of confidence. From an investment perspective, the opportunity has shifted from distressed recovery into normalisation. With inflation anchored, and local market access reopening,

Ghana’s local bond market has been one of the clearest expressions of the stabilisation story in 2025. Yields have compressed sharply over the course of the year, falling from the high-20s to the low-teens, as disinflation took hold and confidence in the policy framework returned.

While much of the easy money has been made, the combination of anchored inflation, a firmer currency and gradual easing still argues for supportive conditions for bonds into 2026, particularly in the mid-to-long end of the curve.

Cote d’Ivoire

Côte d’Ivoire remains one of the most resilient and well-run economies in West Africa. Growth surprised to the upside in 2025 with GDP expanding by 9.7% % in Q2, well above the regional average driven by trade, construction and extractives. The extractive sector should remain a key support next year, with hydrocarbon production ramping up at the Baleine field, rising gold output, and early-stage development of the newly discovered Calao gas field. Public investment under the National Development Plan (2026–2030) should add further momentum, while easing inflation and favourable weather conditions support domestic consumption and agriculture.

(Source: Bloomberg, RenCap Africa)

October’s presidential election was broadly peaceful, reinforcing Côte d’Ivoire’s reputation for relative political stability.

The macro picture has improved meaningfully. Strong export performance up 45% y/y by September this year has pushed the current account into a 0.5% of GDP surplus in 2025, from a previously expected deficit, and driven pooled FX reserves to a record €28.6bn, equivalent to roughly six months of imports. Cocoa price weakness will be a headwind in 2026, but starting buffers are now materially stronger. Fiscal policy remains anchored by the IMF framework. The authorities continue to target a 3% of GDP fiscal deficit in 2026, in line with WAEMU rules, supported by revenue-driven consolidation through tax reform.

Ivorian dollar bonds have already delivered meaningful spread compression in 2025, with the 10-year spread versus US Treasuries tightening from above 500bps earlier in the year to just under 300bps by late 2025

(Source: Bloomberg, RenCap Africa)

On the surface, that move may look crowded. We see it differently. The compression reflects a genuine improvement in macro fundamentals. Growth remains robust across the bloc, fiscal policy is anchored by IMF programmes, FX reserves have risen to record levels, and political risk has declined following orderly elections. In that context, Ivorian bonds still offer an attractive risk-adjusted carry profile into 2026, with further, but more measured, spread tightening likely as macro credibility continues to build.

Egypt

Egypt enters 2026 in a far stronger macro position than it was just eighteen months ago. The March 2024 FX reset was painful but necessary; since then, the adjustment has begun to work. Remittance flows have surged back through formal channels, tourism has recovered meaningfully, portfolio inflows have returned, and FX liquidity has improved. Reserves are back near record highs, confidence has stabilised, and the exchange rate has become relatively stabile.

(Source: Bloomberg, RenCap Africa)

Inflation fell sharply through 2025, reaching a low of 11.7% in September before ticking up to 12.3% in November on administered price adjustments. While inflation is likely to remain above the CBE’s 7% ±2% target band through much of 2026, the broader disinflationary trend remains intact, with further moderation expected in the second half of the year. This has already given the Central Bank of Egypt room to ease decisively, cutting rates by 625bps in 2025. Further gradual cuts are likely in 2026 as policymakers balance supporting growth with maintaining positive real rates.

(Source: Bloomberg, RenCap Africa)

With inflation easing, the EGP supported by FX inflows, and the CBE in a measured easing cycle, local bills and short dated bonds still offer attractive carry without taking unnecessary FX risk.

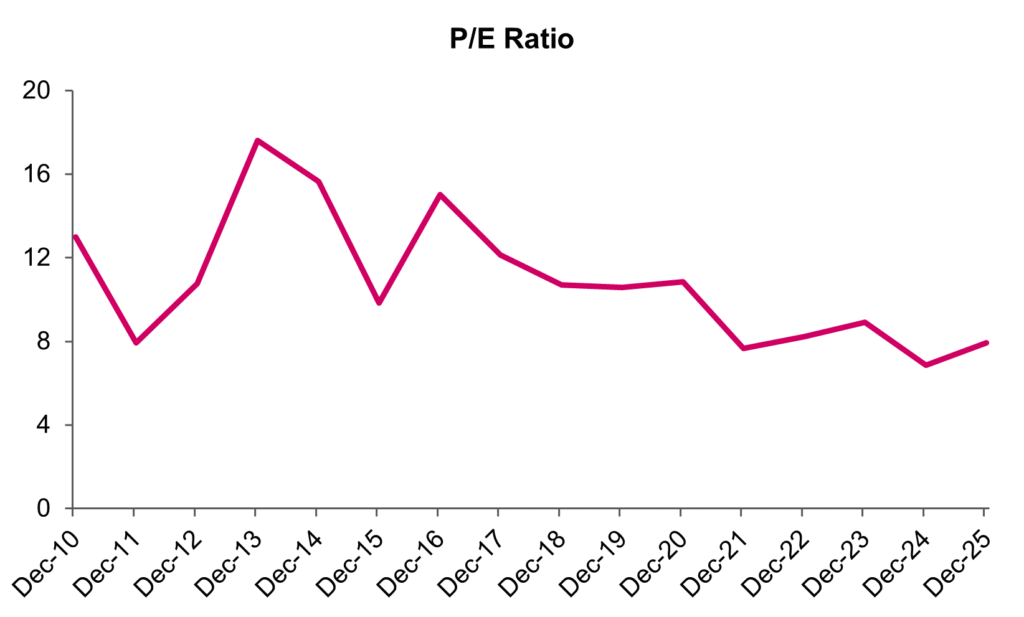

Egyptian equities are trading on a forward P/E of around 7.9x, materially below their 15-year average of 10.9x. That discount is hard to justify in an environment where FX has stabilised, earnings visibility is improving, and the cost of capital is falling.

(Source: Bloomberg, RenCap Africa)

This combination of depressed multiples and improving macro conditions is exactly the type of asymmetry we like.

Africa enters 2026 in a different place from where it stood a few years ago. The opportunity lies in favouring countries where reforms are sticking with clear fiscal discipline and political rrisks are contained. In several cases bonds have repriced but still have value, while equities remain deeply discounted with re-rating still ahead. The key is leaning into dislocation and allocating capital where we see macro improvement is real but not fully priced in. 2026 will be a year of disciplined positioning and if the cycle unfolds as expected, Africa will not remain this cheap for long.