Oil and Gold 2026 Outlook

Black and Gold was a song released in 2008 by an artist called Sam Sparro (one of my favourites at the time). Coincidentally, it came out at an extraordinary moment for markets. Oil had just completed one of the most violent booms–bust cycles in modern history, surging to nearly $147 a barrel on the back of China-led demand growth and a weakening US dollar, before collapsing below $40 as the global financial system seized up. Gold, meanwhile, was only just beginning to reassert itself, setting the stage for the multi-year bull market rising to $1,900/oz by 2011. Showing that faith in fiat money and policy credibility quietly eroded.

Today, the same two assets are again sending distinct signals. Oil looks set to remain range-bound, reflecting a world of adequate supply, cautious demand and geopolitical noise that no longer shocks as it once did. Gold, by contrast, is being repriced as a structural asset formed by who is buying it, how they are buying it, and why. It is this shift in the marginal buyer, particularly across Asia, that underpins the case for gold as we look into 2026.

Gold – The Asians are coming

Gold has had a remarkable year in 2025. Hitting 50 all time highs, and by mid-December, spot prices were up over 60% ytd, while futures were pointing to gains of roughly 65%, forcing many sceptics to revisit old assumptions.

Much of the debate about price revolves around timing and degree of Fed cuts, real rates, or whether the rally has run too far. While fully justified, it misses an interesting and important shift; The marginal buyer of gold is moving East.

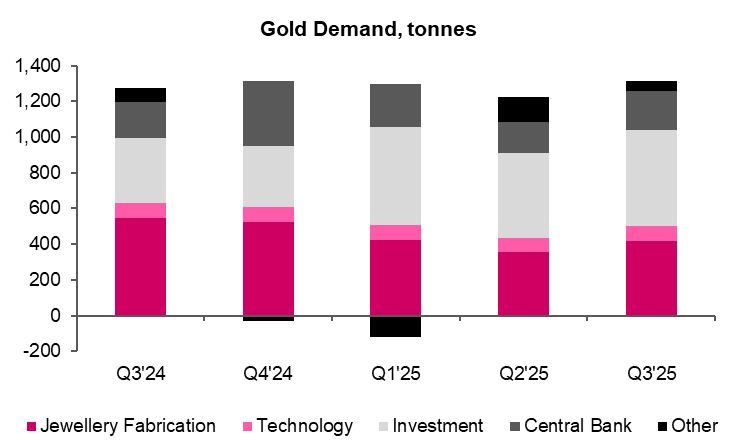

Gold demand rests on four pillars: jewelry, investment, central banks, and technology. Jewelry remains the largest by volume but is highly price sensitive; investment demand is cyclical and reacts fastest to macro shifts; central bank buying is slow-moving but structurally important; and technology demand provides a steady, though smaller, industrial base. As prices rose, the market quietly transitioned from being jewelry-led to investment-led increasingly becoming the driver of the market.

Source: World Gold Council, RCAM.

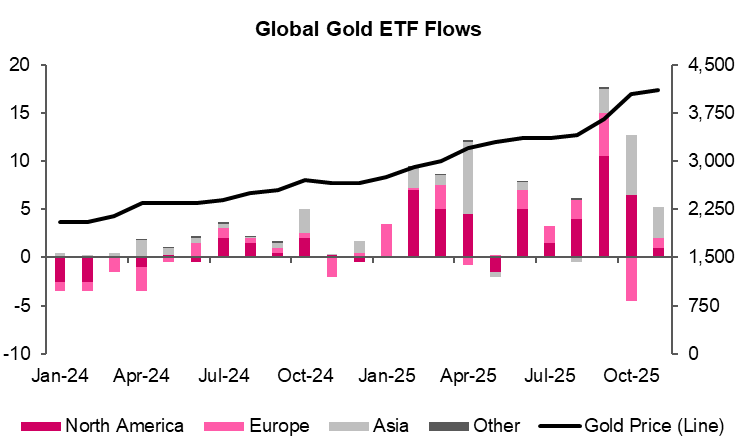

The Chinese government’s announcement of a new VAT reform on gold jewelry, effective from 1 November 2025 through to at least 31 December 2027, has materially altered the economics of traditional retail gold ownership. While gold traded directly on the Shanghai Gold Exchange (SGE) remains VAT-free at the first tier, the treatment of physical withdrawals has become more punitive for non-investment uses. As a result, demand migrated decisively from jewelry toward gold ETFs. In November, total Asian gold ETF inflows reached $3 billion, with China alone accounting for roughly $2 billion. To put that in context, average monthly gold ETF inflows from Asia were approximately $400 million in 2024. By 2025, that average had already risen to around $2 billion per month. November’s Chinese flows alone were five times the entire Asian monthly average in 2024 and effectively matched the whole of Asia’s average monthly demand in 2025.

Source: World Gold Council, RCAM.

With the polity set to run through to December 2027, the rerouting of Chinese gold demand looks like a durable shift to me.

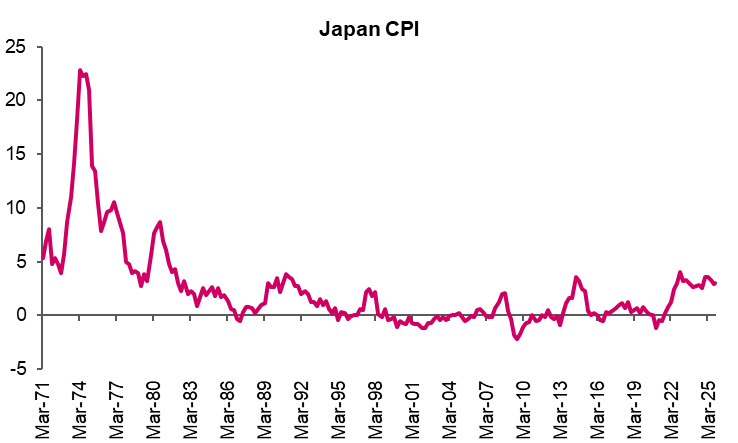

Japan, quieter but powerful leg in the story. Decades of deflation defined household behaviour made inflation hedges unnecessary. In a world of falling or stable prices, cash preserved value, government bonds worked, the opportunity cost of holding a non-yielding asset like gold was real.

Source: Bloomberg, RCAM.

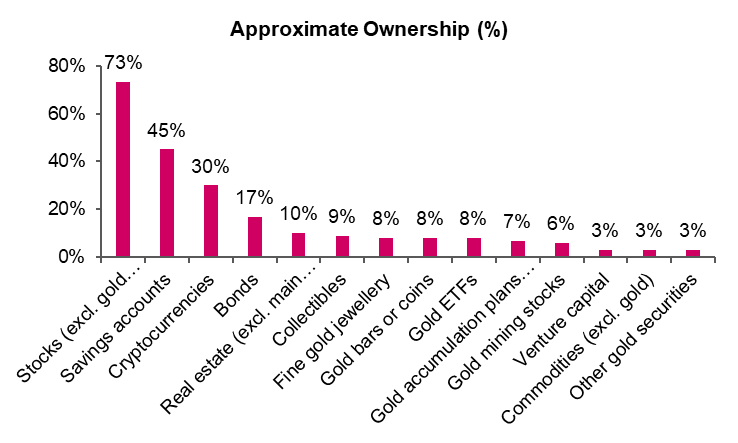

That history is clearly visible in portfolio data today. Gold remains marginal in Japanese portfolios, typically accounting for between 1% and 10% of allocations with the majority clustered at the lower end of that range and very few investors holding more than 20%.

Source: World Gold Council, RCAM.

Cash, bonds, and equities continue to dominate household balance sheets. I believe this will change as Japan enters a sustained inflationary environment, forcing a gradual reassessment of portfolio protection in an economy no longer defined by deflation.

History tells us, “The British are coming!” cried by Paul Revere, was a signal that the balance of power was about to shift. Policy changes in China have redirected demand toward financial gold, and Japan is now at the early stages of a post-deflation regime, both shifts should provide ongoing support for gold prices in 2026.

Oil – An uncertain balance

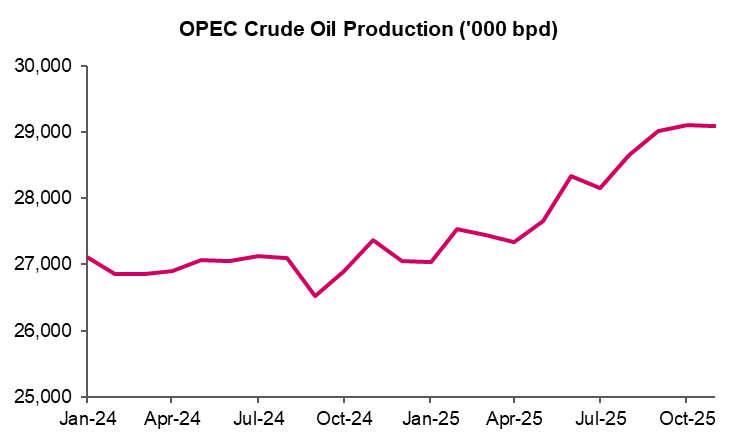

The oil market enters 2026 without a clear directional anchor. The year opened amid renewed trade tensions, elevated geopolitical risks and a shifting global order, with prices largely anchored around USD 60/bbl through much of 2025. The more important surprise came from supply. OPEC reversed years of restraint and returned barrels to the market at a time when many had expected discipline to hold, fundamentally altering the balance just as demand growth began to soften.

Source: Bloomberg, RCAM.

Forecasting oil prices has become about managing ranges. On the downside, a more constructive geopolitical environment, particularly any credible easing of Russia –Ukraine tensions could compress remaining risk premia. That said, Russian crude has continued to find its way into global markets via China and India despite sanctions, suggesting that much of this supply is already priced in. Meaningful downside from here would likely require a material relaxation of sanctions rather than diplomacy alone.

The recent capture of Venezuelan President, Nicolás Maduro, by President Trump’s administration adds to uncertainty around supply. In the near term, the Trump administration’s plan to gradually roll back sanctions that have restricted oil sales would be a positive for the sector. However, the potential for a strong rebound in Venezuela’s output, which has been plagued by decades of neglect, decay and underinvestment, seems limited. Furthermore, the level of investment required, estimated to be in excess of USD100bn (more than 100% of the nation’s GDP), to drive growth in production over the medium term raises question marks on the possibility of significantly higher supply coming to market.

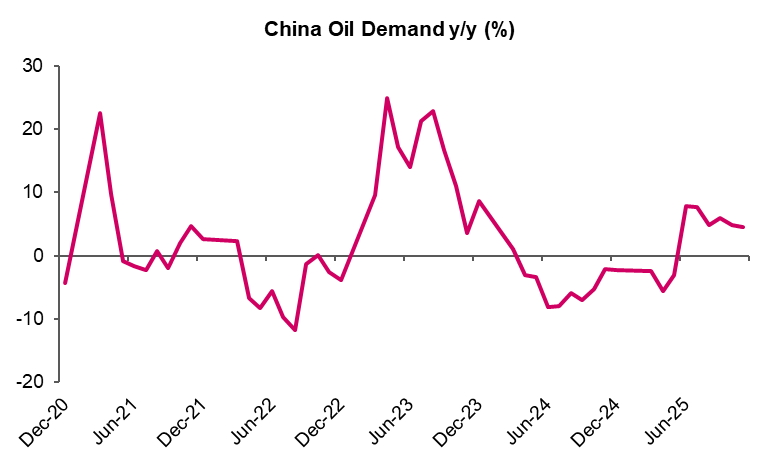

Demand, while still resilient, is slowing. Global oil demand growth of around 1.3% in 2025 masks a structural shift underway in China, where renewable capacity and electric vehicle penetration, now roughly 30% of new car sales, are steadily eroding oil’s role in incremental demand. It is a steady slowdown that becomes more visible over time rather than a sudden drop in consumption.

Source: Bloomberg, RCAM.

At the same time, supply management remains politically and fiscally constrained. Many producers face rising budget pressures and are increasingly reliant on volume rather than price to stabilise revenues, limiting their willingness to cut output even as prices soften. Ironically, this dynamic means that a sharp fall in prices could ultimately prove self-correcting: lower prices would undermine producer economics, curb investment, and force higher-cost supply out of the market, tightening balances again over time.

From an investment perspective, oil in 2026 is more likely to be range-bound and volatility-driven market. We see prices oscillating broadly in a USD 55–70/bbl range under our base case, with downside constrained by supply economics and upside capped by slowing demand and weaker supply discipline.

Oil remains tradable, but not a core conviction asset for 2026. We favour tactical positioning around dislocations rather than long-duration exposure.

Black and Gold revisits two commodities at very different points in their cycle. Oil is range bound, defined by rising supply and slowing demand, while gold is being structurally repriced. China’s policy changes have pushed demand from jewellery into financial gold, and Japan’s slow exit from deflation is beginning to reshape portfolios where gold remains meaningfully under-owned. The result is a durable demand base that should continue to support gold into 2026, even as oil struggles to break out.