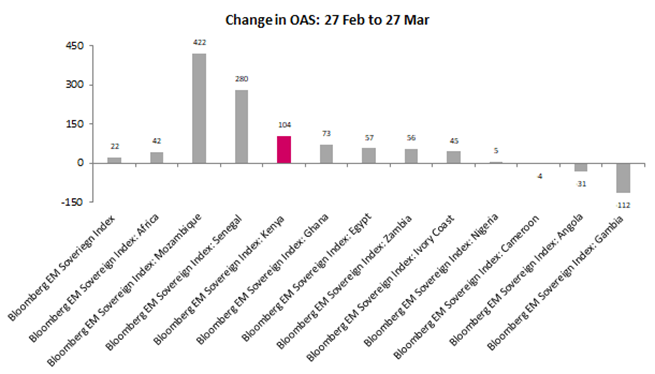

The fallout from the conflict in the Middle East risks materially weakening structural reform efforts by the Kenyan government over the last two years. Eurobond spreads have reacted and Kenya’s Eurobond yields have increased by 104 bps since the start of the conflict—more than the broad EM index and Egypt, and only lower than Senegal and Mozambique.

We believe the Eurobonds are likely to continue to underperform, whilst the local currency is likely to depreciate further, albeit at a slower pace. Investor concern about the sovereign’s outlook continue with questions themed around policy credibility resurface in the absence of an IMF programme. We however believe that the proactive liability management over the last two years by the Kenyan government provides some headroom.

Source: Bloomberg, RCAM

Higher oil prices, fertiliser cost, freight charges and slower tourism to weigh on external accounts

Kenya’s external accounts are expected to be negatively affected by the fallout from the Middle East conflict, particularly as it persists beyond March. The following factors are likely to impact both the current and financial accounts:

- Higher oil prices – Oil prices have risen by approximately 55% since the conflict began, weighing on the nation’s trade balance. Refined oil products account for around 20% of total imports.

- Higher jet fuel prices – The cost of jet fuel has roughly doubled since the start of the conflict, posing risks to tourism, which generated USD 3.5bn in 2024 (2.9% of GDP). Elevated jet fuel costs and weaker demand could also hinder turnaround efforts at the state-owned airline, Kenya Airways.

- Higher fertiliser, freight, and insurance costs – Agriculture (20% of GDP and 50–55% of total exports) is negatively impacted by the surge in fertiliser costs, with Urea and Ammonia prices rising by roughly 50% and 25% respectively. Kenya’s flower industry is reportedly losing up to USD 1.4mn per week due to shipment delays and higher freight costs. Additionally, demand for exports may decline as consumer spending weakens in key markets, whilst reduced spending power abroad may also affect remittances.

- Financing squeeze – Following Kenya’s exit from its IMF programme in April 2025, the government turned to Middle Eastern partners. Although it secured a USD 1.5bn loan deal with the UAE, only USD 500mn was drawn down. Other financing arrangements and fuel import deals from the region also face uncertainty, as Middle Eastern countries may reprioritise resources toward infrastructure rebuilding and defence spending.

Source: Bloomberg, RCAM

Growth, fiscal response, and the 2027 elections likely to widen the deficit

Higher energy and transportation costs pose risks to GDP growth and the cost of living. Rising living costs could trigger renewed protests and social unrest, further weighing on economic activity—a key concern for the incumbent government as general elections approach in roughly 18 months.

There are ongoing discussions around using the road development levy to cap fuel prices in the near term. Prolonged elevated energy prices increase the likelihood that the government may reduce levies and taxes on fuel. Combined with a potential slowdown in tourism and broader economic activity, this will likely lead to lower tax revenue and a higher primary deficit.

Risk‑off sentiment, currency volatility, and inflationary pressures—particularly in housing, water, electricity, gas, transport, and other fuels, which account for 25% of the inflation basket—could push fixed‑income rates higher. When paired with external financing constraints, this may further increase the cost of financing the primary deficit, leading to an even wider fiscal deficit.

Historically, Kenya’s actual fiscal deficits have exceeded projections due to underlying assumptions and slippages. Without an IMF programme and with elections approaching, the deficit could rise over the coming years, contributing to a higher debt‑to‑GDP ratio.

Source: IMF based on WEO as at October 2025, RCAM

Breathing space

The government does have some room to manage pressures on the fiscal and external accounts. Kenya’s economic position improved substantially after being considered a potential post‑COVID default candidate in Sub-Saharan Africa, following Zambia and Ghana. Proactive liability management—supported by the market’s reopening to high‑yield issuers in early 2024—strengthened external accounts and eased refinancing concerns. Gross foreign currency reserves have more than doubled since the start of 2024 to approximately USD 14bn, despite a recent decline. However, fiscal policy inconsistency and the absence of a new IMF programme may pose challenges. A new programme is unlikely to materialise prior the 2027 elections, by which time the full impact of the Middle East crisis will likely have unfolded.

Source: Bloomberg, RCAM