Emerging markets (EM) were a hot topic in 2025 with capital flow marking the strongest year since 2009. Capital flows to US ETFs focused on EM stocks exceeding USD31bn while EM debt funds absorbed more than USD60 billion based on data compiled by Strategas Securities, EPFR Global data.

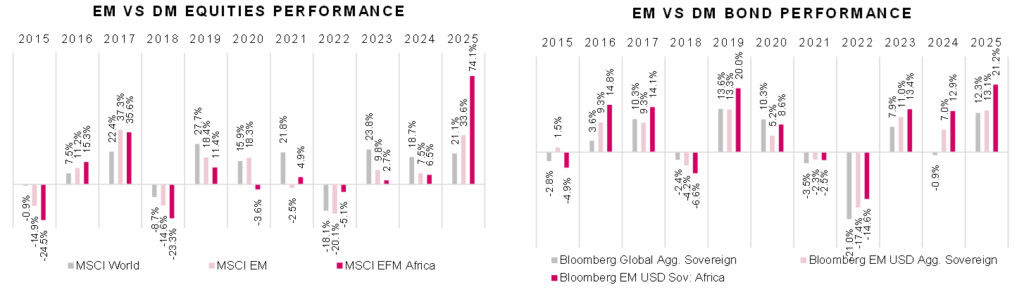

Returns were even more impressive with EM outperforming Developed Markets (DM) by a sizeable distance. The MSCI EM index gained 33.6% outpacing the MSCI World Index, which tracks the performance of large and mid-cap stocks across 23 DM countries, for the first time since 2017. This was a similar case in credit markets, with Bloomberg EM bond index recording its best performance in 2025 since 2019. At first glance the difference between the Bloomberg global aggregate index and EM was not significant in 2025; the outperformance of the Africa sub-index however materially stands out.

Source: MSCI, Bloomberg, RCAM.

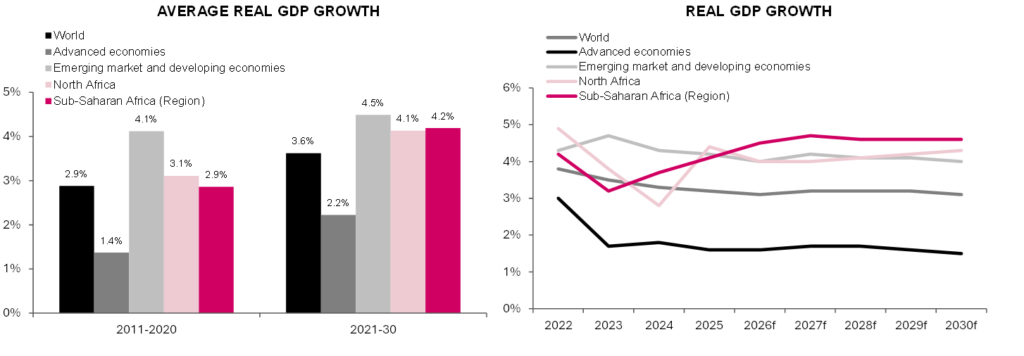

Africa has played a role in this momentum with investors, now more than in recent past, encouraged by recent fiscal reforms, moderating debt burdens, and credible monetary policies in different regions of the continent that have contributed to rating upgrades while economic growth may outpace 2024 levels over the medium term, according to the IMF. As such, investment flows into the region have jumped with hard currency bond spreads narrowing to pre-covid levels, shifting investor attention to local currency investments. The interest in local currency exposure and the boom in precious metals have seen African currencies post record gains and further peaked investor interest in the continent.

Source: IMF, RCAM.

Investors are likely to question whether the resurgence in fundamental and market performance is more than just a recovery from Covid era lows or a turning point for the continent. Systematic factors such as the recent rate cuts by the US Fed and the potential for further weakness of the US dollar, and a growing move to diversify long USD exposures could support the performance of EM as well as African securities. We note that with more developed markets increasingly displaying emerging market type risk factors, particularly on political, fiscal and debt sustainability metrices, the disparities between the two markets are narrowing, which could mean that EM may offer a better risk-return trade-off.

We, however, caution that geopolitical risk could limit investor positioning whilst idiosyncratic risk and uncertainties in different regions and countries could mean the potential for outperformance from the continent will be tested. Skill will be even more required than in recent past to navigate market movements and generate alpha.

A key consideration going forward will be policy credibility, particularly for those IMF programmes coming to an end over the next 12months. Egypt, Ghana, Ivory Coast, and Zambia were supported and benefited from policy credibility and increased access to concessional funding over the last two to three years. In the absence of a funded IMF programme, there will be increased scrutiny on policies going forward and hesitance from investors while access to international capital markets by sovereigns in the region could reduce the willingness for further fiscal reforms.

Sovereigns who have done well implementing challenging reforms without the backing of the IMF, such as Nigeria, could be placed on a higher standing. Question marks will be raised on Ghana and Zambia as their programmes come to an end within the next 12months as well as Kenya, despite the ratings upgrade by Moody’s, has very little chance of a new IMF programme ahead of elections in 2027.

We believe elections over the next 12-18months could be disruptive to fiscal and monetary policy in several countries, including Kenya, but may be less so Nigeria where the 2027 elections already appear to be a one-horse race. Nigeria could fair best in the years to come as it commences monetary easing, maintains ample foreign currency reserves (cUSD46.3bn as at 30 January 2026), prospects for further tax reforms post 2027 and low election risk, which may partly mitigate the need for aggressive election spending, inflation and fiscal pressures.

Angola’s elections, also in 2027, could be a worry for investors given the narrow margin by which the incumbent party secured victory in 2022, the closest ever election since democratic elections were first introduced in the country. Fiscal consolidation efforts by the Angolan authorities appear to have already given way to aggressive spending plans, resulting in expectations of wider deficits in 2025, 2026 and most likely in 2027. Kenya is expected to follow this path, but even more worryingly, given some concerns around debt sustainability although recent liability management exercises have provided some headroom.

Conversely, if we are headed into an even lower oil price environment, with some projecting low USD50/bbl brent oil price by late 2026 on widening global oil surplus, Kenya, like Ghana and Zambia, could benefit from stronger external account performance, all else being equal. Angola, Cameroon and Nigeria will likely struggle in this scenario. The latter could be in a better fiscal, external account and external debt amortization position than Angola, leaving it in a better position to weather the storm. Angola will likely struggle in such a scenario (oil accounts for 55% of fiscal revenues and 95% exports, FX backlog estimated at USD1.8bn as at the end of 2025 according to BFA, and c6% debt amortization to GDP over 2026-28. There is said to be some flexibility on the repayment of Chinese debt, which is part positive, and we expect that approaching the IMF for a funded programme would be deferred till after elections.

For Ghana, one of the star performers and possibly a standout example of debt restructuring with the support of an IMF programme under the G20 Common Framework, could underperform, if we see an aggressive reversal in gold prices, c40% of exports.

We highlight that investor sentiment towards the continent could sour if Senegal, which is still working to secure an IMF programme, eventually restructures its debt. As we write, the Senegalese government continues to speak against a restructuring and highlights its access to the regional debt market, but most metrics (debt to GDP ratio north of 130%) point to the nation’s debt being unsustainable. If a restructuring does not form part of the initial programme, we believe challenges implementing what would be an aggressive front-loaded fiscal consolidation amid political and social backlash would eventually lead to a restructuring. In the same vein, we are watching Mozambique and Gabon closely, although the latter appears to be working towards securing a IMF programme that would support its fiscal consolidation and access to concessional funding to clear its backlog of arrears.

Political risk, especially in the form of coups, will also be a concern for investors given the prevalence in West Africa, the coup in Gabon in 2023, the perceived risk in Cameroon as well as reports of a foiled coup plots late last year.