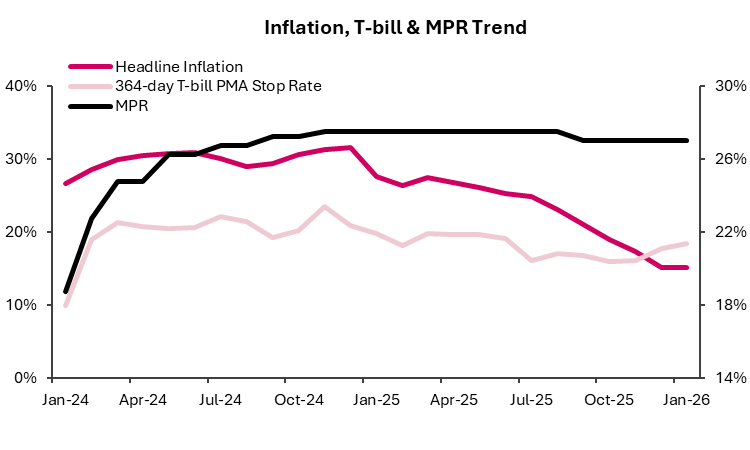

The recent monetary policy committee meeting caught the local fixed income market off guard. At the conclusion of the 304th meeting the central bank governor, Dr. Olayemi Cardoso, announced just a 50bps cut to the monetary policy rate to 26.5% as against consensus expectation of a 100bps moderation. Consequently, there was an aggressive repricing in the local fixed income market with yields immediately trending upwards in the secondary market.

Why the divergence in expectations?

We believe the market had priced in a sharper cut to the policy rate due to the signalling and a sense of “mission accomplished” from the central bank in recent months. Over the past few months, we have seen primary market auction rates decline significantly across most maturities with higher liquidity conditions further suppressing secondary market yields. OMO rates have also decreased close to, if not in line with, T-bill rates.

The rate decision also came on the back of the sizeable slowdown in headline inflation to 15.1% in January 2026 (as against the peak of 31.5% in December 2024) and a 27.5% y-o-y spike in gross foreign currency reserves to USD49.2bn as of 23 February 2026.

Source: Bloomberg, CBN, RCAM

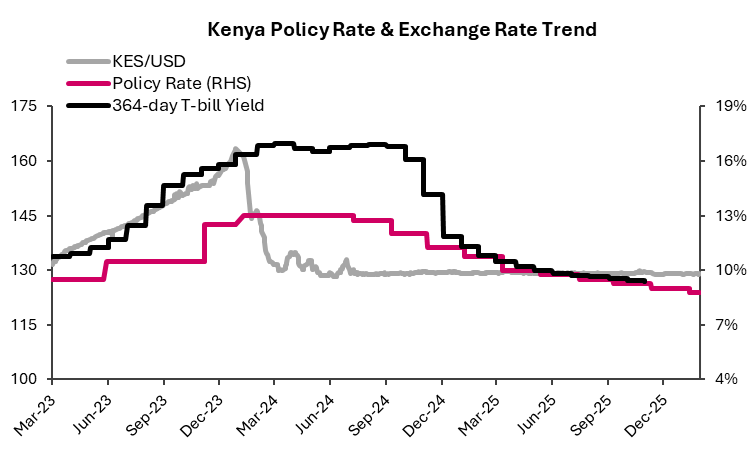

The MPC, however, favoured a more cautious stance as we believe it is still concerned on the inflation trajectory and the overall stability of the exchange rate despite the build up in reserves. The authorities may look to make more frequent and smaller cuts over the next 12months than larger and less frequent cuts. This was a stance taken by the Kenyan central bank (CBK) in 3Q24 following the refinancing of the 2024 Eurobond, appreciation of the Kenyan Shilling and early moderation in yields at the short end of the local fixed income market. The CBK later cut aggressively before siding with several smaller cuts.

Source: Bloomberg, CBK, RCAM

We note that the patient approach with smaller and more frequent cuts may avert knee jerk reactions from market participants, especially foreign portfolio investors, which the central bank is keeping a close eye on. Whilst reserve accumulation provides comfort; we see the central bank trying to avert a rush for the exit that could be the case with a larger reduction to the policy rate.

For local investors, this could mean a slower passed decline in yields over the next 12 months, providing an entry opportunity for those yet position for the duration play.

Where do we go from here?

The next MPC meeting is pencilled in for May 2026, which will give the central bank sufficient time to assess inflationary pressures as well as the exchange rate. The currency has gained c6% YTD and c11% y-o-y at the official market to NGN1350/USD levels, with some locals linking the slowdown to less demand during the Chinese New Year. The spread to the parallel market has narrowed in recent weeks following the re-inclusion of bureau de change entities into the official market to access dollars.

We expect there will be ample time for the central bank to publish its net foreign currency position, hopefully in detail, and this we expect will play a material role in how foreign and local investors further position in 2026.