Senegal is a divisive subject amongst stakeholders who are torn on whether the government will restructure its debt as part of a new funded IMF programme. A crucial signal on the road ahead will be the amortisation payment of EUR333mn on its 2028 Eurobond due on 13 March 2026. It would not be logical for the government to make this payment, even with the capacity to do so, if it plans to announce a debt revamp in the coming months.

The government currently has lost access to international capital markets, with the domestic regional capital markets providing a much-needed source of funding and protecting the sovereign from default. There is, however, uncertainty on the continued appetite of regional fixed income investors with demand skewed to shorter dated maturities. The lack of market access could pressure regional foreign currency reserves, which stood at USD33bn, as at the end of October 2025.

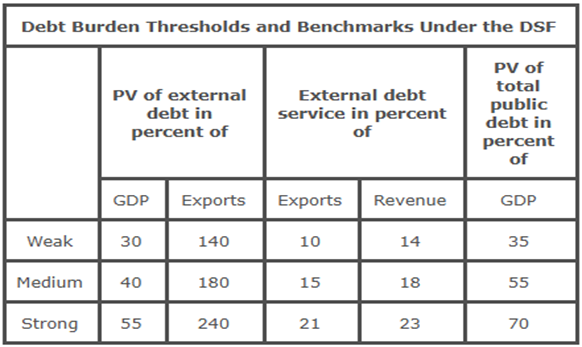

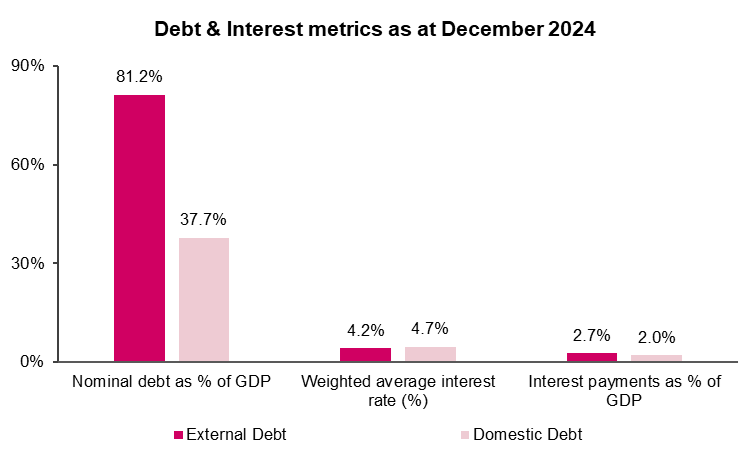

We still do not have a clear picture on the nation’s debt mix, post discovery of the hidden debt but the government should be in breach of one (PV of central government debt stood at 110% of GDP as of December 2024), if not two of the IMF’s low-income country debt sustainability framework.

Source: IMF and RCAM

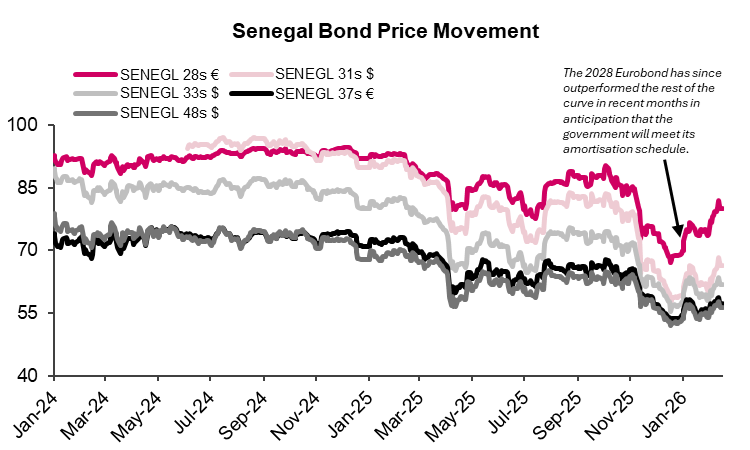

The Senegalese authorities and the Fund have so far failed to reach a staff level agreement on an eagerly anticipated programme. This combined with the Prime Minister (PM) Sonko’s defiance towards a debt revamp initially trigged a sharp decline in bond prices in October, but similar pronouncements more recently seem to have lost their shock factor.

Source: Bloomberg, RCAM

The PM believes the Fund should have spotted the now well-known hidden debt during past programme reviews and visits, a view shared by some stakeholders. As such, the belief is that the burden and blame should be shared in a way that should not result in a debt restructuring.

It is important to note that towards the end of 2025, the Senegalese government were moving forward with economic policies, such as an unexpected plan to cut energy costs. This is viewed as contradictory to what would have been supported by the IMF.

Investors are concerned on this standoff as negotiations on a new programme show little signs of progress since conversations moved past corrective actions.The IMF’s New Mission Chief for Senegal held in-country meetings last month raising some hope for clear path going forward.

The bumpy road ahead

We anticipate a protracted and challenging road to a new programme. The government could be positioning to blame the Fund for any potential debt restructuring and austerity measures on the horizon.

The defiance and combative stance of the PM is reminiscent of Ghana, who lost access to the international markets in 2021. The Ghana government eventually reached a staff level agreement with the Fund in December 2022, five months after the initial call from the President Akufo-Addo to the IMF. This was more than a year after the then finance minister resisted calls to seek an IMF bailout and a debt revamp.

Nonetheless, we expect the Senegalese government to maintain its reliance on the regional market and alternative, albeit narrowing financing options, to meet financing needs. The absence of a clear and credible economy policy direction from the Faye-Sonko administration thus far means limits the potential for growth-neutral fiscal consolidation.

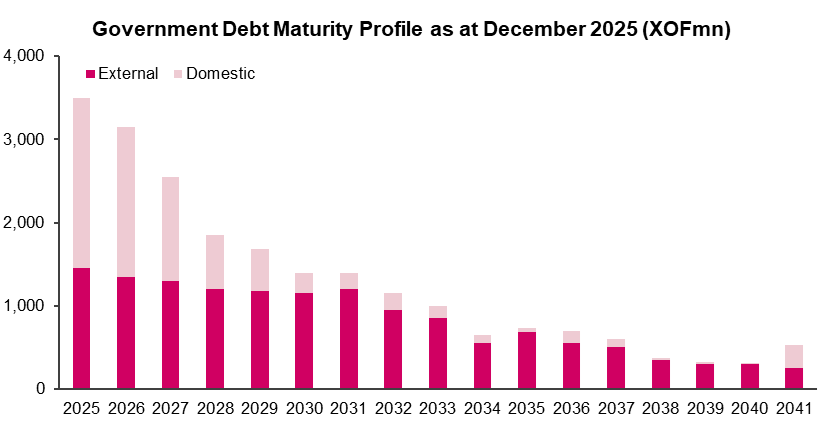

Source: DDP, TDMS tool, Ministere des Finances et du Budget, RCAM

A possibility that would hit credibility

There is a world whereby Senegal and the IMF reach a deal on a new programme without a debt restructuring. This would involve the Fund expressing a view that the nation’s debt is sustainable on a forward-looking basis with a heavy front-loaded fiscal consolidation as a key input.

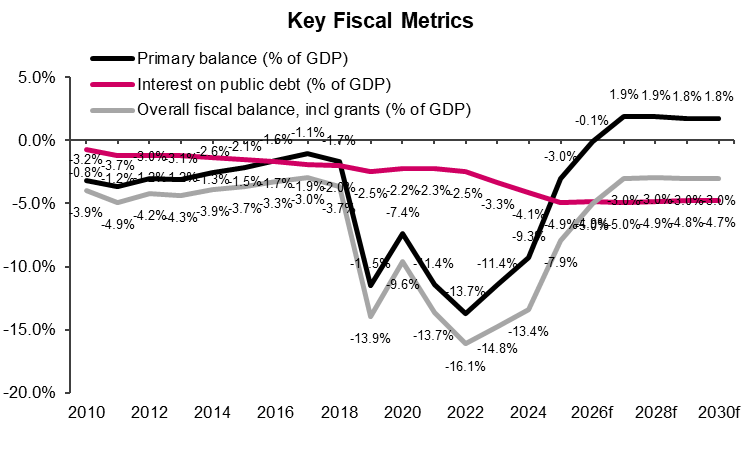

Source: IMF, RCAM

Such an agreement may initially be met with a positive response by the market, but sentiments would sour given concerns on how challenging the austerity measure would be for the Senegalese government to implement amid a tense social backdrop. Furthermore, the decision by the Fund may renew concerns on its objectivity and the influence of politics in its decision making on the continent following the recent failed programme in Kenya.

Regardless, we believe a funded programme would eventually lead to a restructuring after the first review, which could occur in early 2027. This path would be a negative for the IMF but more so the Senegalese government who would eventually have to embark on a long restructuring exercise under the G20 Common Framework at a later point in time. Furthermore, a more aggressive fiscal consolidation trajectory could risk economic growth, cause some social unrest and impact the political ambitions of the Faye-Sonko administration.

We note that a stumbling block to a funded programme from the IMF without a restructuring could be the unwillingness for bilateral partners to support the agreement. This would hinder the ability for the Senegalese government to refinance its maturities at lower interest rates providing some fiscal space.

The credible option that would suit everyone

A clearer and credible path ahead would be for the government to reach a staff level agreement with the IMF with a debt revamp path as part of the programme sooner-rather-than-later. The Senegalese government may reject now but may eventually have to accept as financing options narrow even further as policy credibility deteriorates.

The restructuring could focus on external debt given how testing and large the impact of domestic debt revamp would be across the region, which could spell sizeable haircuts for Eurobond holders. Furthermore, with a pegged currency, Senegal will not be able to inflate away some of its local debt suggesting a slower, more painful recovery than was the case in Ghana. This persistent economic strain is poised to diminish political support for the Faye-Sonko administration as the 2029 election cycle approaches.

Source: Ministere des Finances et du Budget, RCAM

Regardless of the path followed in the next few weeks and months, it will likely be a test of both the credibility of the IMF and the Senegalese government.The risk of social unrest is high on all the paths ahead with the extent dependent on timings of a potential restructuring as this will influence the level of pain felt in the economy.